Best Way to Build Credit After Buying a House

How to Build (or Rebuild) Credit

Maintaining proficient credit is vital in order to brand important purchases downward the line. If you need tips on how to build credit, continue reading to learn more.

Past Janet Berry-Johnson, CPA

Reviewed past Lauren Bringle, AFC®

Whether you're looking to build credit for the start time or rebuild bad credit afterwards a few money missteps, y'all're probably facing a common conundrum: y'all demand credit to have a credit score, but you lot demand a proficient credit score to get canonical for loans and credit cards.

So what is the all-time way to build credit?

The best way to build credit is to focus on the v major factors that affect your credit score, like paying your bills on time, keeping your credit utilization low, not opening too many new credit accounts in besides short a time and using all types of credit responsibly.

In this guide, we'll explore how to overcome this "Catch-22" of credit, how to build good credit, why it's of import to build credit and how you tin employ it responsibly.

Table of Contents

- How to establish credit

- How to build credit responsibly

- Why build adept credit?

- How long does it take to build credit?

- How long does it take to rebuild credit?

- How can I build credit fast?

- Good credit could save you - big fourth dimension

- Tin savings accounts impact your credit score?

- Do debit cards or prepaid cards help y'all build credit?

- Exercise rent or utilities affect credit?

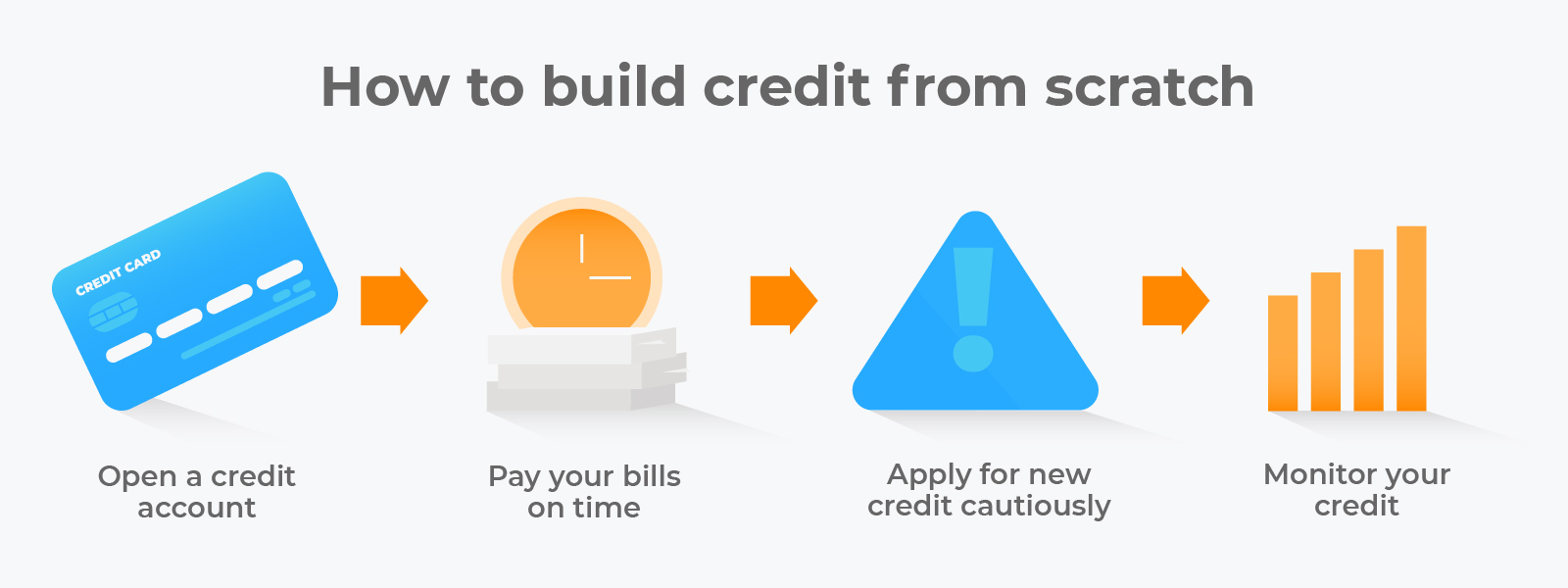

How to build credit from scratch

Ready to learn how to build credit fast? Let's launch correct in. If y'all're new to credit and need to institute credit from scratch, here are a few things yous can exercise to get started:

i - Open a credit business relationship

The first step in learning how to start credit is to open a credit account. You may have to start with a secured credit card or a credit architect loan if you currently have bad credit or don't accept any.

The very first time you lot apply for credit, the lender volition order a credit report and review your credit history. That showtime inquiry establishes your credit report.

2 - Pay your bills on fourth dimension

This includes everything from credit cards and loans to rent payments, utilities, and cell phone plans. Even accounts that aren't unremarkably reported to a credit bureau can negatively impact your credit score if they're referred to a collection agency. Paying bills and credit carte debt on fourth dimension could help to avoid bad credit later on.

3 - Use for new credit charily

When yous utilise for new credit, the lender will run a credit check, resulting in a "hard inquiry" on your credit report. Difficult inquiries bring downward your credit score, especially if yous open several new lines of credit within a short time frame.

If you lot're shopping for a loan, such as an auto loan, personal loan, or mortgage, credit rating agencies wait you to shop around for the best rates. For that reason, a financial institution will ignore multiple inquiries for the aforementioned type of loan made within a xxx twenty-four hours period.

4 - Monitor your credit

Get in the habit of checking your credit written report regularly. Clarify it for inaccurate information and dispute whatsoever wrong information with the credit reporting agency immediately.

Ultimately though, building credit is more of a marathon than a sprint – it just takes time. In fact, credit scoring company FICO requires someone to accept at least six months of credit history earlier they will even calculate their credit score.

What is the best way to build credit responsibly?

While we've covered the general rules for how to build credit, let's go into some more specific tools you lot use to build it. The first step in building credit is to apply for your first credit account.

For many people, their first credit awarding is for a credit menu. Merely without any credit payment history, you may not qualify for one of the major credit carte issuers such as Visa or MasterCard. The practiced news is, there are other means to get started. Acquire how to establish credit without a credit card.

Here are 7 alternatives to traditional, unsecured credit cards:

- Shop card

- Secured card

- Credit architect loans

- Certificate of Deposit-insured loan

- Educatee loan

- Co-signer

- Authorized user

1 - Store carte

Retail store cards have a reputation for blessing applicants with no credit. You lot're more probable to become accepted for a card that tin but be used at one store, or a group of stores, than a card that can be used anywhere.

To get started with a retail store card, ask your favorite retailer most their options, or bank check out this post on the 5 best store credit cards to build credit. Make sure to ask the card issuer about the interest rate, monthly payment options, and other important details earlier signing upward.

two - Secured credit bill of fare

Secured credit cards crave a security deposit and ofttimes give you lot a credit line equal to your deposit. Once you lot start using the credit builder card, the issuer sends you monthly statements. If you don't pay your bill, the issuer can take the money you owe from your deposit.

In one case you've demonstrated you can handle your menu responsibly to your credit card visitor, the card issuer may allow yous to have a higher credit line than your deposit or upgrade to an unsecured card and refund the eolith.

3 - Credit builder loans

Credit architect loans are another option for building credit.

Like to a secured credit card, many lenders that offer credit architect loans collect a deposit and give yous a credit limit equal to the deposit amount. Your eolith goes into a savings account that you cannot admission until you've fully repaid the loan. Equally long as you pay as agreed, the lender sends a favorable study to the credit bureaus.

You can find these types of loans at a local credit marriage, or through Cocky, which is the first company to make these types of loans available online or via mobile app in all 50 states. Another positive about choosing Cocky? You don't have to brand a security deposit to be approved for the loan.

four - A Certificate of Deposit-insured loan

A Certificate of Deposit (CD) is a financial product similar to a savings business relationship, but y'all agree to proceed your money with the depository financial institution or fiscal institution for a fixed period of time. In return for letting the banking company hold onto your coin, you receive higher involvement rates than y'all would from a savings account.

To apply that CD to build credit, some banks permit you use the funds in your CD as collateral for a loan. The loan shows upward on your credit written report as a secured loan, and helps you build credit when you brand on-time payments. Credit unions sometimes telephone call these share-secured loans.

five - Student loans

Getting approved for federal pupil loans does non depend on credit, but managing your pupil loans well will impact your credit score.

Remember, whether you lot make your payments on fourth dimension, make your payments belatedly, or miss your payments completely, your payment history on educatee loans gets reported to the credit bureaus.

6 - Co-signer

If you tin can't get canonical for credit on your own, you may have a parent or other shut relative who is willing to co-sign on a loan in your name. Having a co-signer with excellent credit may assistance yous go a lower interest rate than you would on your ain.

As you lot brand on-fourth dimension payments, you build your credit. However, if you default (don't pay) on your account, the lender will go later on your co-signer to collect the debt.

To get a credit menu completely on your ain, yous must be at least 21 years old. While you tin can go a carte equally young as 18, at that age you must either have a co-signer or proof of steady income to qualify.

However, if y'all're under age 18 and want to start edifice credit, your parents may exist able to add you every bit an authorized user on their credit card. Users over the age of eighteen can also accept advantage of being an authorized user.

Banks accept their ain minimum historic period requirements for adding a pocket-sized equally an authorized user, so parents should phone call the number on the dorsum of their card to ask nigh historic period requirements. For more, see our guide on establishing credit when you're 18.

If you do this, exist sure to pick a relative that has a potent credit score, a history of on-time payments and low credit utilization. Becoming an authorized user on an business relationship with a history of missed payments could impairment your score rather than ameliorate it.

Why is it important to build good credit?

Good credit plays a vital role in your fiscal life. Most people remember of good credit for obvious reasons similar getting a credit carte, car loan or mortgage. But credit can play a role in less obvious things like renting a auto, apartment or abode; getting approved for a prison cell phone contract, and perhaps even getting a job.

When yous apply for a loan or charter, the lender wants to see a credit reference to run across if you'll be able to responsibly manage the money they lend you by paying them dorsum on fourth dimension. Some employers bank check credit references besides, especially when the job you're applying for involves handling money or dealing with confidential fiscal information.

The most common blazon of credit reference is a credit report from one of the 3 major credit bureaus – TransUnion, Equifax and Experian. Your credit report includes information about your past and existing credit accounts. It outlines how much you owe, how long you've been using credit, and whether you lot consistently brand on-time payments.

Your credit score, on the other hand, is like a form that's given to your credit report.

How long does it take to build credit?

In that location's no 1 answer for how long it takes to build your credit. It depends on a number of private factors, including the types of credit you're using, the balances owed and the credit scoring model in utilize.

According to Experian, information technology can take at to the lowest degree iii-6 months of activity earlier a credit score tin be calculated. In one case you have a score, it can fluctuate oftentimes. According to TransUnion, your creditors will likely report to the credit bureaus every 30-45 days.

So every month, your credit score can go upwards or downward depending on how well yous manage your credit.

How long does it take to rebuild your credit?

Rebuilding a damaged credit score can be tougher than starting with a blank slate, just it is possible.

The first pace is to cheque your credit study to run into exactly where you lot need to improve. If y'all're trying to rebuild after bankruptcy, you may demand to apply for a secured credit card to start rebuilding.

If your issue is missed or late payments, piece of work on bringing your accounts upwards-to-engagement and set upwards reminders so you lot pay your bills on time going frontward. If your credit utilization ratio is as well loftier, create a plan to pay downwards your debt and get your credit utilization rate down to 30% or less.

A bankruptcy stays on your credit written report for 7-10 years, merely you lot can meet an improvement in your credit score much sooner. Only put in the work to rebuild your score and keep in mind the five factors that become into a credit score adding listed afterwards in this post.

Whether you're new to credit or trying to undo the damage caused past by credit mistakes, building credit takes fourth dimension. In a nutshell:

- Don't accuse more than you tin afford to repay

- continue balances low

- set up reminders to pay your bills on time

These actions show that you know how to use credit responsibly and you'll exist rewarded with a stiff credit score.

How tin I build credit fast?

If yous're trying to purchase a home or get a car loan, waiting 3-6 months for a credit score may seem like a lifetime. You might be looking for a mode to speed upwards the process.

Your power to build credit fast depends on your starting point. If you lot take no credit, building an excellent credit score apace may be difficult. In this case, you may have to apply for a secured bill of fare and demonstrate your ability to make on-time payments for a few months before you can utilize for an unsecured carte or movement onto other credit products.

If you've been using credit for a while, how fast you tin meliorate your FICO score depends on whether your credit report contains negative data and the age of those adverse events.

A tardily payment within the last three months will take a greater impact than a tardily payment two years ago.

Assuming you already accept a credit file and don't have any recent negative marks on your credit study, hither are 6 ideas for improving your score speedily:

1 - Review your credit report

Dispute any errors that might be dragging your score downward, like late payments or credit limits that appear lower than they actually are.

2 - Pay your bills on time

Your payment history accounts for 35% of your average credit score, so make your payments on time every calendar month. Also, a tardily or missed payment could stay on your credit study for upwards to seven years.

three - Pay downwards your balance

If you lot have revolving credit accounts with high balances, or carry a credit card balance month-to-calendar month, pay them down as soon as possible. 30% of your credit score is based on the corporeality you owe, and then paying downwards large credit menu balances can have a big bear upon in a brusque period of time.

4 - Get a credit card or two

If you don't have any open credit cards, apply for i or 2. Get a secured menu or get an authorized user on a relative'due south account if you tin can't get canonical for one on your own.

v - Utilize your cards sparingly

Remember, most credit experts recommend keeping your utilization rate below 30% - both on a per-card ground and in total. So utilize your cards, but don't employ them too much.

For case, allow's say you take two credit cards with a credit limit of $1,000 each. Yous might charge up to $250 on each card and pay the credit card balance in full each month. This volition keep your utilization charge per unit under 30%.

vi - Raise your credit limit

If you already have a credit carte, try calling the company and asking them to raise your credit limit. This automatically decreases your credit utilization rate and improves your score.

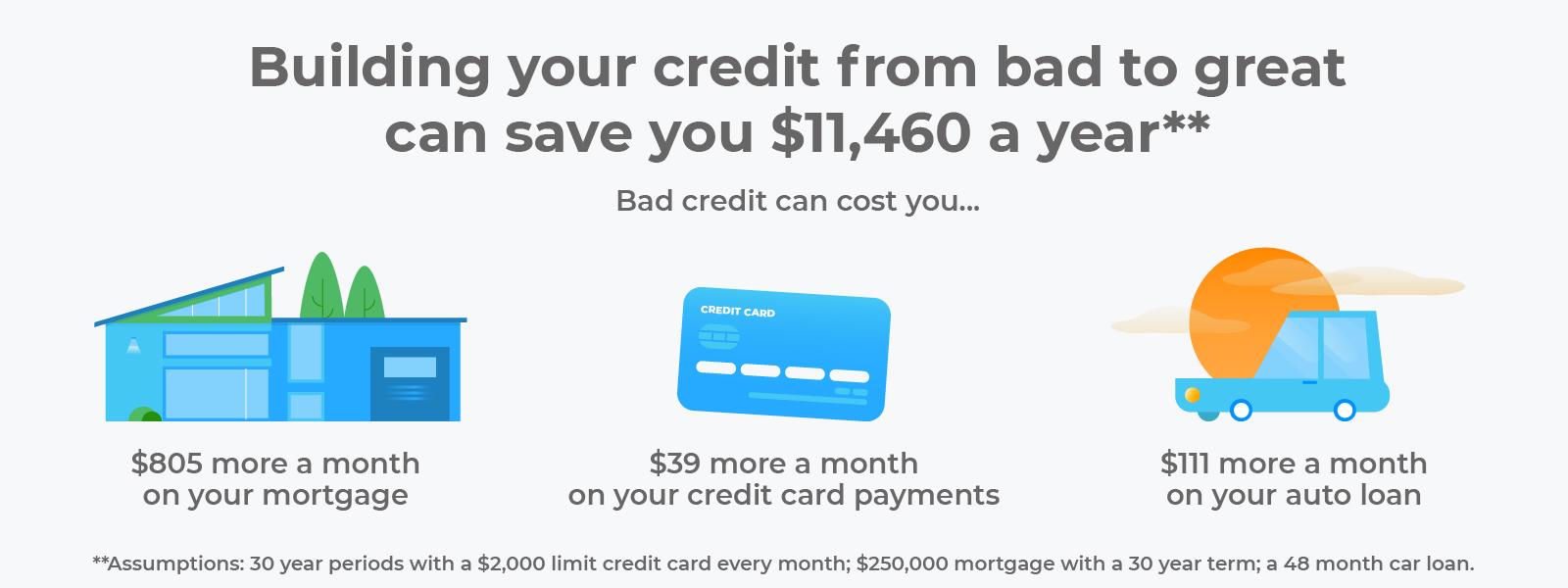

Expert credit could save you, big time

A good credit score non simply makes it easier to go credit, it tin as well save you lot thousands of dollars over your life. Let's walk through an example in which you're planning to accept out a $250,000, 30-yr stock-still charge per unit mortgage.

According to myFICO'south Loan Savings Computer, with a FICO score of 760 to 850 (an Excellent score), the Annual Percentage Rate (APR) on your mortgage could be around iv.291%.

If your FICO score dropped to somewhere betwixt 680-699 (a Off-white credit score), your APR could be 4.695%.

That doesn't seem like a huge difference, but over the term of a thirty-twelvemonth loan, the lower credit score would toll yous $21,595 in additional involvement payments.

The skillful news is that building solid credit is not a mystery, every bit long as you sympathise the fundamentals.

Can savings accounts affect your credit score?

Savings accounts don't directly affect your credit history because they're non listed on your credit report.

That doesn't hateful it's not important to save or that they can't impact you when you're trying to get a loan. Besides your credit score, a lender will nigh probable prefer to run into you take something in savings since information technology increases the risk you can pay them dorsum.

Having savings puts you in a stronger position to manage any debt or credit products you have (credit cards in particular). A savings account makes it less likely that y'all have to turn to a credit card or payday loan for an emergency expense.

Practice debit cards or prepaid cards help credit?

Yous might be wondering nearly ii types of cards that aren't included on the above listing: debit cards and prepaid cards. While these cards might expect and swipe similar credit cards, they won't help you build your credit.

When you use a debit card, the funds are taken directly from your depository financial institution business relationship, so the transaction is treated as a greenbacks buy, even if you choose "credit" instead of "debit" at the time of sale.

When you use a prepaid card, you're spending money y'all loaded onto the menu in advance.

Both debit cards and prepaid cards have a card network logo like Visa, MasterCard, American Express or Discover on them, only you're non borrowing money.

Credit cards yet, are basically using borrowed money. They allow you to buy now but pay later, study your credit history to the credit bureaus and affect your credit score.

Debit cards and prepaid cards are not reported to the credit bureaus and won't have any effect on your credit score.

Exercise hire or utilities affect credit?

Other bills you pay typically don't directly affect your credit score, either. Monthly payments for rent, backyard services, and utilities, for instance, typically don't appear on your credit report because the company doesn't written report data to the credit bureaus. If you don't pay your bill and your account is turned over to a collection agency, still, that drove will impact your credit score.

That is changing, nonetheless. Experian, one of the three major consumer credit bureaus in the U.S., launched Experian Boost, to incorporate rent and utility payments to assistance heave your credit score (assuming yous're paying them on fourth dimension, of course).

Use credit to build credit

Merely put, building credit means building credit history. It means having credit accounts, such as credit cards and various types of loans, using them responsibly over fourth dimension and paying them off as agreed.

Substantially, credit is a grade of trust with financial institutions. As you build credit, y'all build trust with potential lenders over time, making information technology more than probable they would be willing to lend you money in the time to come.

Want to build your credit? Become the Self app to get started.

Sources:

- Insider. "How to build credit with credit cards and better your credit score — whether you're starting from scratch or already an expert". https://world wide web.businessinsider.com/personal-finance/how-to-build-credit-with-a-credit-card-steps

- The Rest. "vii All-time Means to Build Practiced Credit". a href="https://www.thebalance.com/means-to-build-adept-credit-960109">https://world wide web.thebalance.com/means-to-build-good-credit-960109

- Money Fit. "How to Build Credit: A Step-by-step Guide". https://moneyfit.org/building-credit

Nigh the author

Janet Berry-Johnson is a Certified Public Accountant and personal finance author with a groundwork in accounting and finance. See Janet on Linkedin and Twitter.

About the reviewer

Lauren Bringle is an Accredited Financial Advisor® with Self Financial– a fiscal technology company with a mission to help people build credit and savings. See Lauren on Linkedin and Twitter.

Editorial Policy

Our goal at Self is to provide readers with current and unbiased information on credit, fiscal wellness, and related topics. This content is based on inquiry and other related articles from trusted sources. All content at Cocky is written by experienced contributors in the finance manufacture and reviewed by an accredited person(s).

Source: https://www.self.inc/blog/how-to-build-credit

0 Response to "Best Way to Build Credit After Buying a House"

Post a Comment